About

About Us

Quality Assurance

Grain Trading

Seed Supply

Organic Grain Supply

Vision Portal

Contact Us

Careers

GrainCorp

Grains

GrainCorp AU

Saxon

Bulk Handling

CropConnect

Animal Nutrition

Animal Nutrition AU

Animal Nutrition NZ

Human Nutrition

Human Nutrition

Oilseeds

Pin and Peel

Energy

Energy

Auscol

Sustainability

Ventures

About

About Us

Quality Assurance

Grain Trading

Seed Supply

Organic Grain Supply

Vision Portal

News

Contact Us

Careers

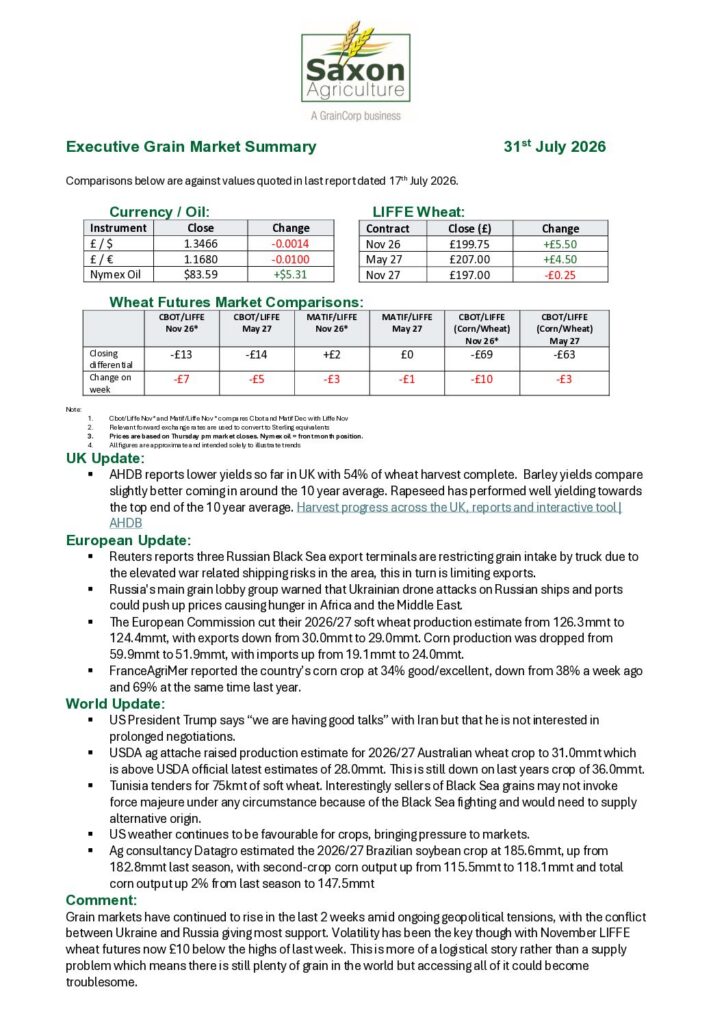

Weekly Executive Summary

July 31, 2026

Related News

View all news

Executive Summary

Weekly Executive Summary

Weekly Executive Summary

Ready to buy or sell?

Seeds or grain, conventional or organic, we’re here to help maximise your ROI.

Speak to our specialists